Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

If you’re shopping for a home in San Jose right now, you’ve probably heard someone mention appraisal gap coverage. It tends to come up after a house gets ten or fifteen offers and everyone starts wondering why one buyer won over another.

The good news? It’s not nearly as complicated as it sounds.

Here’s what it means, why sellers care about it, and how to decide if it’s something that makes sense for your situation.

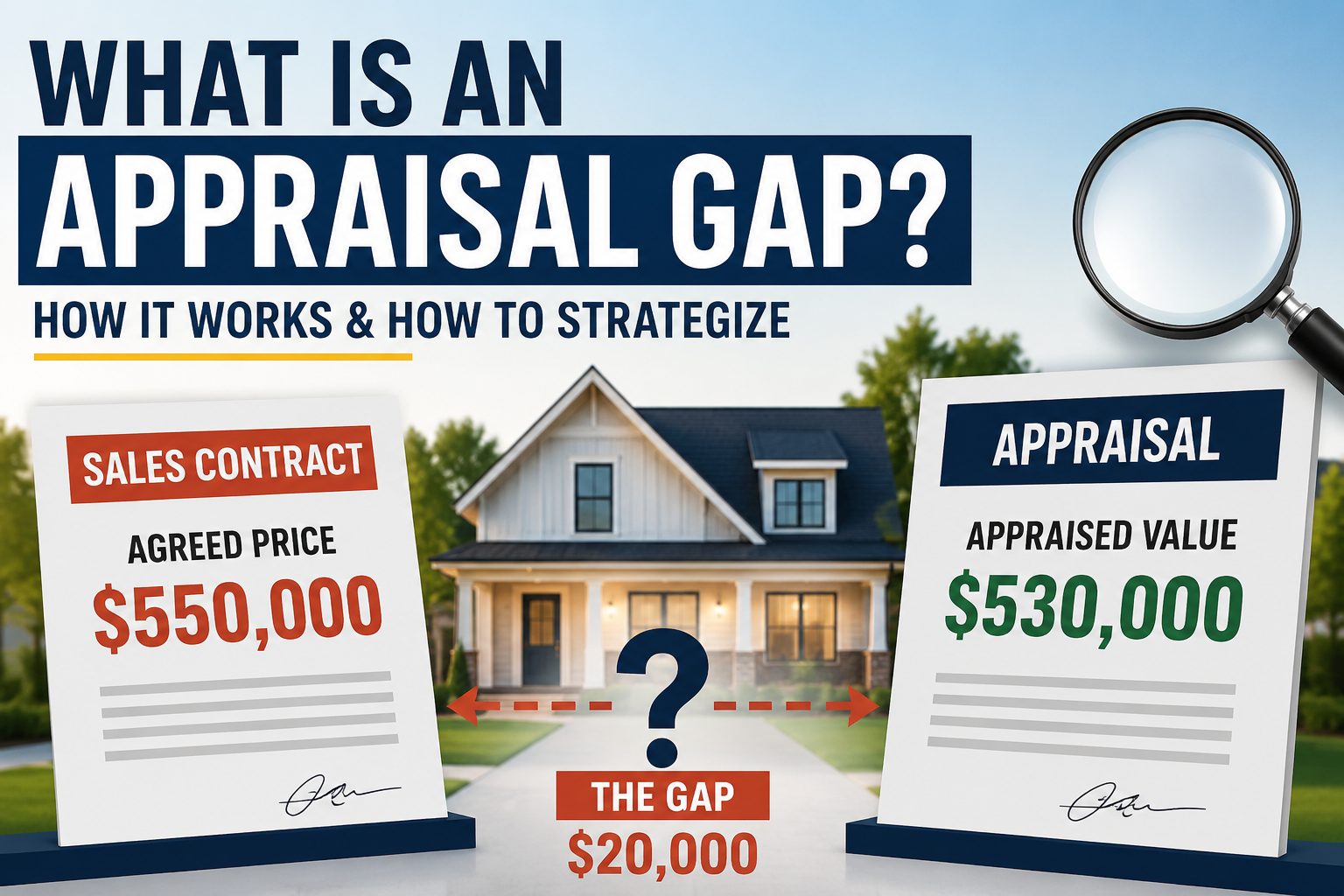

First, what is an appraisal gap?

After your offer is accepted, your lender orders an appraisal. The appraiser’s job is to determine what the home is worth based on recent comparable sales—not on how competitive the bidding war was.

That’s where things can get interesting.

In neighborhoods like Willow Glen, Almaden Valley, and throughout San Jose, it’s common for homes to sell well above the asking price. But the appraisal doesn’t always keep up with those aggressive offers.

If the appraised value comes in lower than your purchase price, the difference is called the appraisal gap.

For example, imagine you offer $1,850,000 on a home listed at $1,700,000. A few weeks later, the appraisal comes back at $1,780,000.

That leaves a $70,000 appraisal gap.

Why does that matter?

Because your lender isn’t going to base your loan on what you offered—they’ll base it on what the home appraised for.

So if you planned to finance the purchase with a traditional mortgage, the bank will lend against the $1,780,000 appraised value, not the $1,850,000 purchase price.

That $70,000 difference doesn’t just disappear. Someone has to cover it.

Without a plan in place, buyers often have to renegotiate with the seller, bring in additional cash, or, in some cases, walk away from the transaction.

So what is appraisal gap coverage?

Appraisal gap coverage is simply a promise you make in your offer.

You’re telling the seller:

“If the appraisal comes in low, I’m willing to bring in extra cash to cover some—or all—of the difference.”

From a seller’s perspective, that’s reassuring. It means your offer is less likely to fall apart because of financing.

There are a few different ways buyers handle it.

Full appraisal gap coverage

You agree to cover whatever the difference ends up being, no matter how large it is.

This is very attractive to sellers, but it also carries the most financial risk.

Capped appraisal gap coverage

Instead of leaving it open-ended, you set a limit.

For example, you might agree to cover up to $50,000 if the appraisal comes in low.

This is one of the most common approaches because it makes your offer stronger while still protecting you from an unexpectedly large shortfall.

Waiving the appraisal contingency

Some buyers remove the appraisal contingency altogether.

That means they’re committed to buying the home at the agreed price regardless of what the appraisal says.

It’s one of the strongest offers you can make—but also one of the biggest financial commitments. Before going this route, it’s important to understand exactly what you’re agreeing to.

How do you know how much gap coverage to offer?

There’s no magic number.

Instead, it comes down to your finances and your comfort level.

Here are a few questions worth asking yourself before you submit an offer:

- Do you have enough cash beyond your down payment and closing costs to comfortably cover an appraisal gap if one happens?

- Is the home intentionally priced below market to attract multiple offers? If so, there’s a greater chance the final sale price could outpace the appraisal.

- What’s the highest price you’re truly comfortable paying for this home?

That last question is especially important.

It’s easy to get caught up in a bidding war, but it’s much easier to make smart decisions when you’ve already established your limit before the offers start flying.

If you offer appraisal gap coverage, how do you protect yourself?

You don’t have to leave yourself completely exposed to stay competitive.

A few simple steps can make a big difference:

- Consider putting a cap on your appraisal gap coverage instead of agreeing to unlimited coverage.

- Talk with your lender ahead of time so you know exactly how much cash you’ll have available if the appraisal comes in low.

- Make sure you understand the language in your purchase contract. If the appraisal comes in much lower than expected, it’s important to know what protections you still have and what your obligations will be.

These are conversations worth having before you submit an offer—not after it’s been accepted.

The bottom line

Appraisal gap coverage isn’t just another piece of real estate jargon. It’s a real financial commitment that can absolutely make your offer more competitive in today’s market.

But it should never be a number you choose in the heat of a bidding war.

Know your budget. Know your limits. Understand the market you’re buying in. And make sure your offer reflects what you’re comfortable with—not just what it takes to win.

If you’re buying a home in San Jose, Willow Glen, Almaden Valley, or the surrounding area, I’d be happy to walk through the numbers with you and help you put together an offer that’s both competitive and financially responsible. Feel free to reach out anytime.

Blog Footer

GET YOUR FREE HOME SELLING BOOK

About the Author – Michelle Elliott

With over 20 years of experience navigating the fast-paced Silicon Valley market, I provide a strategic, results-driven approach to residential real estate. My career is built on a foundation of deep local expertise and a relentless commitment to my clients’ success, resulting in over $235 million in lifetime sales volume and a consistent ranking in the top 3% of agents in Santa Clara County and top 2% at Coldwell Banker. My expertise has been featured on KTVU Fox 2, Real Producers and the Willow Glen Resident. She is also the co-host of the San Jose Podcast “Say What You Want About Real Estate”

A Hyper-Local Expert with Global Reach

I specialize in San Jose, in the neighborhoods of Willow Glen (95125 & 95124) Cambrian Park and Almaden, Downtown San Jose/Japantown (95112) markets. As a certified Luxury Property Specialist with Coldwell Banker Realty, I combine high-end marketing strategies with granular neighborhood knowledge to help my clients achieve premium results.

The “Tiger” at the Negotiating Table

My clients have characterized me as a “tiger” at the negotiating table who remains “sweet and patient” with my clients throughout the process. I pride myself on being a fierce advocate for my buyers and sellers, ensuring the best possible terms in every transaction, and I strive to be the best Realtor in 95125! This balance, drive, and tenacity have earned me consistent 5-star ratings across Google, Zillow, Realtor.com, and Yelp.

Michelle Elliott

Michelle@michelleelliottrealtor.com

1712 Meridian Ave, Ste C, San Jose, CA

DRE 01777533

(13 × 1 in) (45 × 1 in) (6 x 1 in) (1 x 1 in)")